Borrowing business in the US may not be easy and the requirements to be eligible, length of time taken in taking the loans and the interest rates charged can present a major challenge to many small businesses due to the challenges in obtaining the loans. Traceloans.com is a solution to this problem, as it will help business people to find appropriate lending sources by matching them with one or more lenders.

This guide will assist small business owners to know how Traceloans.com functions, what to expect when applying, and make wise decisions that can enable them to get the funding they need to grow and operate.

What is Traceloans.com?

Traceloans.com is a web based company that provides small business owners with a network of lenders that provide them with a variety of financing options. Although it is not a direct lender, it acts as an intermediary, which makes the process of obtaining a loan easier. The platform will ease business lending by connecting borrowers with the right lenders via their requirements and financial portfolios.

Borrowers have to ensure that they check the credentials of the lenders they are associated with via Traceloans.com. The United States is a state where all lenders are licensed and subject to state and federal regulations. To avoid falling victim to scams and deplorable loan agreements, it is always important to verify the legitimacy of the lender and their legality before giving out personal and financial information to them.

Why Business Owners Search for Traceloans.com Loans

Proprietors of small business frequently utilize Traceloans.com to satisfy urgent financial requirements like making rent, buying equipment, paying wages, or financing growth initiatives. The platform provides rapid solutions to online loans, which may be especially helpful when it comes to covering gaps in cash flows or using timely growth opportunities.

Nevertheless, one should be careful. The interest rates and other fees charged on fast online loans may be high resulting in huge sums of money being repaid. Thus, the cost of taking loans and the inability to pay back can be easily avoided by properly reading the loan conditions and fully comprehending their expenses.

Traceloans.com and Credit Score Considerations

A credit score is a major determinant in accessing a business loan via sites such as Traceloans.com lenders will compare it against your creditworthiness to determine whether you get a loan and the terms and conditions.

A credit score of 670 or higher would immensely lower borrowing expenses. An example is that 60 to 80 points might help your loan have an interest rate that is 5 to 15 percentage points lower which would save you thousands of dollars in the long run.

We should verify your credit score prior to applying. This will enable you to correct any errors and get to know about your financial position so that come the time to apply, you are all prepared.

How Business Loans Work in the US

Banks, credit unions, and online lenders are the providers of business loans in the U.S., each of which has its peculiarities:

Banks: Banks are usually cheaper in regard to interest rates but demand good credit background and a lot of paperwork.

Credit Unions: The Credit Unions can be more personalized and offer competitive rates, though they can have membership requirements.

Online Lenders: Provide quicker approvals and other more relaxed terms, which is open to a wider spectrum of companies.

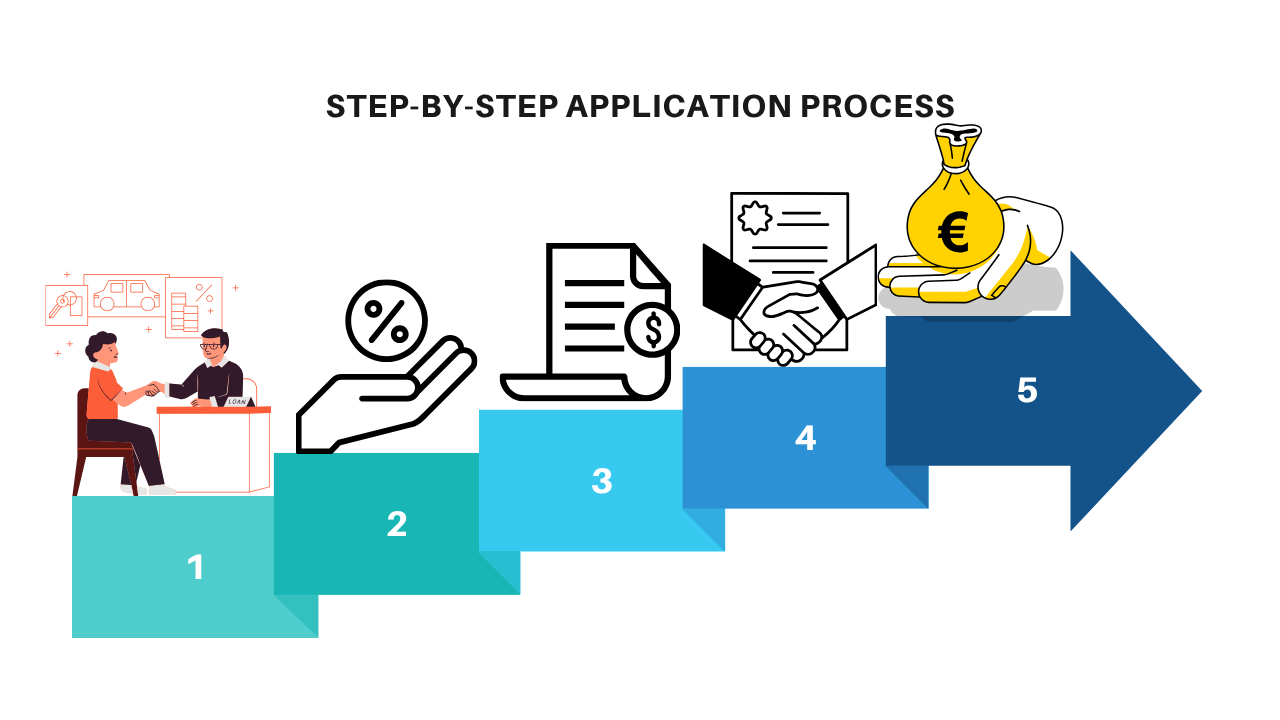

Step-by-Step Application Process

When you apply to take a business loan with Traceloans.com there are several important processes that will be followed with the aim of getting the right type of funding that will meet your requirements. The following is a brief overview on how to do it:

1. Determine Loan Amount and Purpose

Make it clear as to the amount of funding you need and what it is that you need it for- whether it is purchasing equipment, working capital or expansion. This is clear enough to choose the appropriate type of loan and lender. An example would be the working capital loans which would be used to meet the day to day expenses and the equipment loans which would be used to meet the purchase of machinery.

2. Evaluate Your Credit Score

Determine your Personal credit as well as your business credit score because it largely determines loan access and terms. Better interest rates and conditions on loans can be the result of higher credit scores. You can use free resources to test your scores and correct any discrepancies before using them.

3. Prepare Necessary Documents and Compare Lenders

Prepare the necessary materials, including tax returns, financial statements and business plan. Traceloans.com can also help you to compare different lenders in order to secure a match with the one that best suits your business requirements. Make sure that you know the requirements and terms of each lender.

4. Submit Application and Review Terms Carefully

Ease out the loan application form and provide all the necessary papers. When the loan is approved, carefully analyze the loan terms such as the interest rates, repayment terms and any fee. Get an explanation on anything that is not clear.

These steps will help you increase your likelihood of receiving a business loan which will be in line with your financial needs and goals.

Risks of Online Loan Platforms

Online lenders have the benefit of being convenient, although they are not without their problems as they present a risk to the borrowers. Most of them have high-interest rates and other hidden fees that may make repayment expensive. There are even fake websites that are out to steal personal or financial information. The other issue is privacy of data, which is not a strong point of all platforms, exposing sensitive company and personal data.

To prevent scams, one should ensure the lender is licensed and regulated, no up-front fees, read all terms of the loan, and use secure websites with an https and padlock. Caution is a way of securing your business and money when accessing online loan facilities.

Read Also: JAA Lifestyle Login 2025: Easy Access, KYC, and Earning Tips

Benefits of Using Traceloans.com for Business Owners

There are a number of benefits to using Traceloans.com as a business owner who wants to finance his business:

Fast Loan Approval

The loan application at Traceloans.com is so simplified that it will allow quick approvals and provision of capital within fast periods, sometimes even within 1-3 days. The quick turnover is especially useful to companies that have an urgent demand on money.

Ability to Apply from Anywhere

The site is fully internet-based, and the business owner can apply to take a loan anywhere without the necessity of going to the bank or other financial institutions in person.

Access to Multiple Lenders

Traceloans.com introduces borrowers to a group of lenders, and the probability of obtaining good terms and conditions of loans depending on the unique business requirements.

Potential to Improve Credit Score

Obtaining and repaying a loan with Traceloans.com will help the business owners record as financially responsible and their credit scores may ultimately go up.

Saving Time for Business Operations

The effectiveness and rapidity in loan application process saves the business owners time to concentrate on business operations as opposed to time wastage in massive paper work and approval processes.

These advantages render Traceloans.com an attractive choice among business owners who want to get convenient and effective financing sources.

Final Word

Traceloans.com is a convenient service that can be used by business owners to find a range of lenders and ease the process of finding financial support needed for various purposes. Though it takes quick approvals and it is flexible, the borrowers must first compare terms, ensure that the lender is credible and is aware of all charges before applying. Sound borrowing habits and research may assist small business organisations in getting the necessary funding they require and reducing financial risks as well.

Read More: 401k Contribution Limits 2025: What You Can Save This Year